Everything you need to know about an FHA Loan

If you’re buying your first home, you’ve probably heard the term “FHA loan,” especially if saving a large down payment feels challenging.

For many first-time buyers in New England, an FHA loan can be the bridge between renting and owning. But it’s not perfect for everyone.

Let’s break down what an FHA loan is, how it works, and when it might make sense for you.

What is an FHA loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA).

Important: The FHA does not lend you money directly. Instead, it insures the loan, which protects the lender if you default. Because of this protection, lenders are willing to offer more flexible approval standards.

This is why FHA loans are especially popular with first-time buyers.

Why FHA loans appeal to first-time homebuyers

Lower down payment requirements

One of the biggest barriers to homeownership is saving for a down payment.

With an FHA loan:

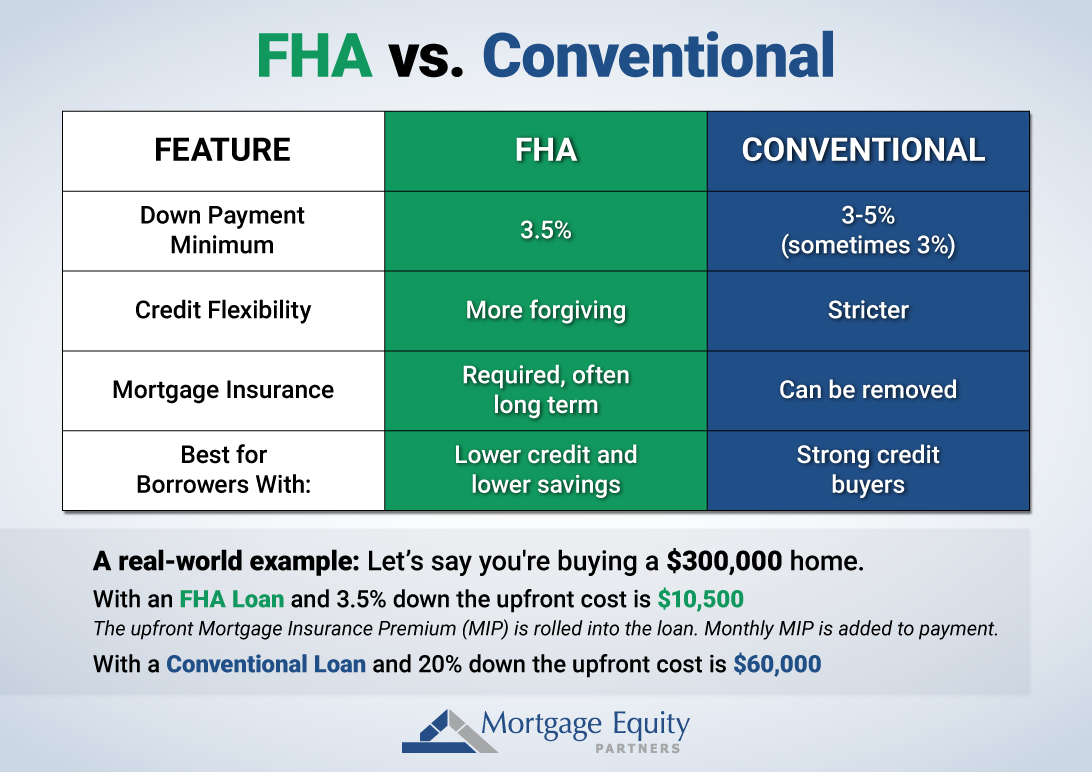

- You can put down as little as 3.5% if your credit score is 580 or higher.

- If your score is between 500–579, you may still qualify with 10% down.

Compare that to traditional advice about needing 20% down, which isn’t realistic for many first-time buyers.

More flexible credit requirements

FHA loans are more forgiving if:

- You have limited credit history

- Your score is lower than ideal

- You had past financial challenges

Many conventional loans prefer scores above 620–640, but FHA loans can be more flexible.

That flexibility makes FHA a strong option for recent graduates, buyers rebuilding credit, and buyers with higher student loan balances.

Higher debt-to-income flexibility

FHA loans often allow higher debt-to-income (DTI) ratios than conventional loans.

This can help if:

- You have student loans

- You have a car payment

- Your income is solid but your monthly obligations are higher

For first-time buyers early in their careers, this flexibility can make qualification possible.

How FHA mortgage insurance works

Here’s the trade-off: FHA loans require mortgage insurance.

There are two types:

Upfront mortgage insurance premium (UFMIP)

Typically 1.75% of the loan amount and usually rolled into the loan.

Annual mortgage insurance premium (MIP)

Paid monthly. The amount depends on loan size and down payment.

Unlike conventional PMI, FHA mortgage insurance often lasts:

- The life of the loan if you put down less than 10%

- 11 years if you put down 10% or more

This is one reason many buyers later refinance into a conventional loan once they build equity.

When an FHA loan makes sense

An FHA loan may be a good fit if:

- You have a credit score below about 700

- You don’t have a large down payment saved

- You want to become a homeowner sooner rather than later

- You plan to stay in the home several years

- You’re buying a modestly priced primary residence

It can be especially helpful if waiting to save 20% would take many more years.

When an FHA loan may not be ideal

You may want to consider conventional if:

- Your credit score is 700+

- You can put down 5–10% or more

- You want mortgage insurance that can be removed sooner

- The home price is near FHA loan limits in your area

Also, FHA loans have property standards. The home must meet certain safety and livability requirements, which can limit fixer-upper options.

FHA loan limits

FHA loans have maximum loan amounts that vary by county. In high-cost areas, limits are higher. In lower-cost areas, they’re lower.

Before shopping, check your county’s FHA loan limit so you know your ceiling.

The bigger picture for first-time buyers

An FHA loan is not about getting a perfect mortgage. It’s about getting into the housing market and building equity. If done correctly it helps to create financial stability and start long-term wealth building.

Many homeowners use FHA as a stepping stone and refinance later when their credit improves or equity grows.

Final thoughts

An FHA loan can be a powerful tool for first-time homebuyers in New England who:

- Don’t have a large down payment

- Have less-than-perfect credit

- Want flexible qualification guidelines

But it’s not one-size-fits-all.

Before deciding, you should compare FHA and conventional quotes, ask a qualified lender for total monthly payment comparisons and consider how long you plan to stay in the home.

The best loan isn’t the one with the lowest down payment. It’s the one that supports your long-term financial stability. If you are ready to take the next step, start the pre-approval process today or reach out to one of our knowledgeable loan officers to learn more about FHA loans.